Price forecast from 27 to 31 January 2025

-

Energy market:

The new American administration has started running around the buffet and taking away each other’s leftovers. The food is not for inward consumption, but to throw at everyone at once: Russia, China, and Canada. All of them. They have such a national sport: throwing food. Soon they’ll go to the bathroom and start looking for something to throw. When you have no brains, you’re happy. You can’t even realize how stupid you are. Eating cakes, dancing with checkers, and having a ball on the catwalk while calling everyone to Mars. It’s a rare madness, rare. Hello to the analysts in the Kremlin. They should be drunk with excitement.

All that steam will blow a whistle in a couple of days. And the world will see the helplessness of an old log. Hello!

Yeah, and the call from Washington to Denmark didn’t go well. They’re not willing to sell anything to anyone. Wow. Why is that? Ha-ha-ha-ha.

This release was prepared with the direct participation of analysts from trading platforms eOil.ru and IDK.ru. Here is an assessment of the situation on the global and Russian markets.

What are we waiting for? Judging by the intensity of the US autocratic behavior, a black mark will be sent to OPEC next week. “Either you raise production, or… we’ll release a new blockbuster where we show you how we are.” Somehow that’s how this will play out. The situation is thinning. Why? Because Washington doesn’t have enough excitement for everyone. The beads (Apple phones) are selling worse and worse, but there will be someone to dance on. Iran, for example. But nothing much will happen there, because everything that will be extracted in Iran will go to China. Bottom line: Brent below 75.00 is utopia at the moment.

If the KSA and the UAE just drag on dancing to Washington’s tune (they will not increase production), there are chances of a crisis in the U.S. before the new president finishes his cake. Expensive resources will provoke a new round of inflation, which will lead to an increase in the Fed Funds rate, a fall in the stock market, and impeachment. Inability to impose their ideas, if they were still sensible, discrepancy between deeds and words, spending resources on dark deeds in other countries (in the same Europe: sanctions, duties, threats, military bases) all this will lead to the fact that one day you will see that 300 million fat people are unable not only to dominate the rest of the thin people, for example, from Holland, but even to maintain their own existence.

The Indians seem to bend to Washington and Russian oil sales to this country will fall. But this phenomenon is unlikely to last for a long time. Moreover, China will not completely cut its purchases from Russia, if it officially reduces them. And India and China are two very angry neighbors of each other. Delhi needs an eighth-generation cardboard war elephant, and it cannot be created in a declining economy. China has made a sixth-generation fighter jet. That’s competition.

Grain market:

Without a new pandemic, the grain market is not able to grow much. In addition to the pandemic, there is a possibility of blocking grain supplies from Russia, but this will be extremely difficult to do, as both Africa and Asia are, let’s be blunt, very much interested.

It is difficult to talk about the weather, yes, Russia will not have a harvest like last year, and even more so the year before, as there is no or little snow in the Volga region, but we will get our 75 million tons of wheat somehow.

The bulls in the grain market should not expect a strong price increase due to optimistic forecasts for the gross harvest in the world. Trade wars will also not be able to cause significant damage to food supplies, because if there is a surplus somewhere, it will be offered on the world market at a discount and quickly dispersed to importers.

USD/RUB:

It is worth recognizing that the American negative impact on the sale of Russian resources has its place. But it also shows once again that there is no point in living under Washington.

Most likely our exports, and at the same time our imports, will contract in FY25, which will not lead to a major distortion in the foreign exchange market.

Yes, most likely, after the correction, which is underway at the moment, the pair will continue to gravitate towards 115.00. However, the growth above this mark is still questionable.

We are forced to note that if defense spending remains high, inflation will continue to rise moderately, averaging just over 1 percent per month in 2025.

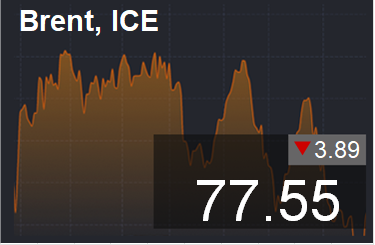

Brent. ICE

Let’s look at the open interest volumes for Brent. You should take into account that this is three days old data (for Tuesday of last week), and it is also the most recent data published by the ICE exchange.

At the moment there are more open long positions of asset managers than short ones. Over the past week the difference between long and short positions of asset managers increased by 7.5 thousand contracts. The bullish positions have been growing for a month. Sellers have started to run away. Bulls continue to increase their control.

Growth scenario: we switched to February futures, expiration date is February 28. We are waiting for a pullback to buy. The movement target is 84.00.

Downside scenario: we stay out of the market. It is possible to sell from 84.00.

Recommendations for the Brent oil market:

Buy: on a pullback to 75.00. Stop: 73.80. Target: 84.00 (94.00).

Sell: on approach to 84.00. Stop: 84.80. Target: 75.00.

Support — 73.88. Resistance — 79.12.

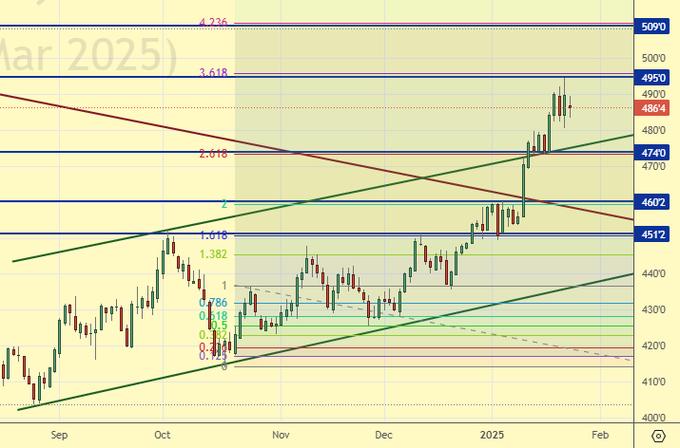

WTI. CME Group

US fundamentals: the number of active rigs decreased by 6 to 472.

U.S. commercial oil inventories fell by -1.017 to 411.663 million barrels, with a forecast of -2.1 million barrels. Gasoline inventories rose by 2.332 to 245.898 million barrels. Distillate stocks fell -3.07 to 128.945 million barrels. Cushing storage stocks fell by -0.148 to 20.655 million barrels.

Oil production fell by -0.004 to 13.477 million barrels per day. Oil imports increased by 0.621 to 6.745 million barrels per day. Oil exports rose by 0.437 to 4.515 million barrels per day. Thus, net oil imports rose 0.184 to 2.23 million barrels per day. Oil refining fell by -5.8 to 85.9 percent.

Gasoline demand fell -0.239 to 8.086 million barrels per day. Gasoline production fell -0.043 to 9.237 million barrels per day. Gasoline imports fell -0.11 to 0.34 million barrels per day. Gasoline exports rose -0.02 to 0.993 million barrels per day.

Distillate demand rose by 0.269 to 4.108 million barrels. Distillate production fell -0.473 to 4.71 million barrels. Distillate imports rose 0.07 to 0.289 million barrels. Distillate exports rose 0.205 to 1.329 million barrels per day.

Demand for petroleum products fell by -1.076 to 19.597 million barrels. Petroleum products production fell by -1.864 to 20.317 million barrels. Petroleum product imports rose 0.134 to 1.691 million barrels. Exports of refined products rose by 0.278 to 6.657 million barrels per day.

Propane demand fell -0.02 to 1.577 million barrels. Propane production fell -0.026 to 2.605 million barrels. Propane imports rose 0.052 to 0.201 million barrels. Propane exports fell -0.101 to 1.76 million barrels per day.

Let’s look at the WTI open interest volumes. You should take into account that this is three-day old data (for Tuesday of last week), and it is also the most recent data published by the CME Group exchange.

At the moment there are more open long positions of asset managers than short ones. Over the past week the difference between long and short positions of asset managers increased by 11.2 thousand contracts. Buyers left in small volumes, while sellers decided to retreat more pronouncedly. Bulls keep control.

Growth scenario: we consider the March futures, expiration date is February 21. We have encountered a pullback. We will buy when approaching 71.00

Downside scenario: there is no sense to sell yet.

Recommendations for WTI crude oil:

Buy: when approaching 71.00. Stop: 69.70. Target: 83.00.

Sale: no.

Support — 71.57. Resistance — 75.80.

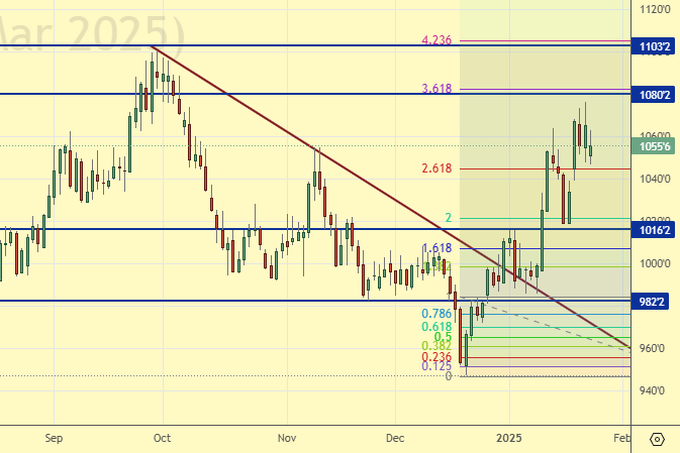

Gas-Oil. ICE

Growth scenario: we consider February futures, expiration date is February 10. We are waiting for a pullback to 680.0 where we will buy again.

Downside scenario: most likely we will not see deep levels. Off-market.

Gasoil Recommendations:

Buy: when approaching 680.0. Stop: 670.0. Target: 900.0.

Sale: no.

Support — 688.25. Resistance — 726.75.

Natural Gas. CME Group

Growth scenario: we consider February futures, expiration date is January 29. The market scares us with failures, but we do not give in. We hold the long. We move the stop order along the trend.

Downside scenario: we don’t think about sales yet.

Natural Gas Recommendations:

Buy: no. Those in position from 3.354, move your stop to 3.780. Target: 5,000.

Sale: no.

Support — 3.721. Resistance — 4.365.

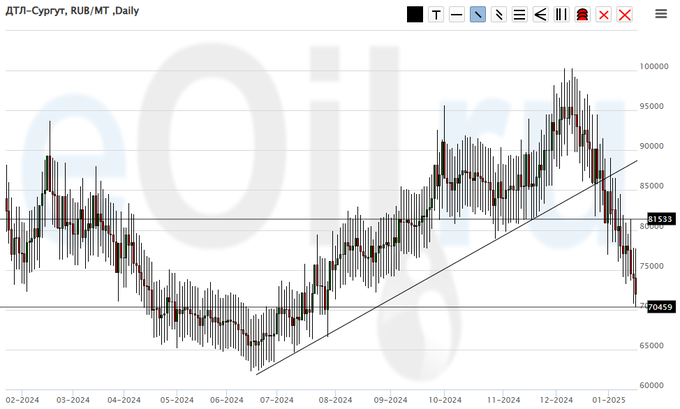

Diesel arctic fuel, ETP eOil.ru

Growth scenario: we should buy here. Technically, the situation is favorable.

Downside scenario: we will not sell anything. There is a constant risk of a sudden rise in prices.

Diesel Market Recommendations:

Buy: Now (72000). Stop: 68000. Target: 110000.

Sale: no.

Support — 70459. Resistance — 81533.

Helium (Orenburg), ETP eOil.ru

Growth scenario: it makes sense to buy here. It is unlikely that the company will release helium cheaper. This is most likely the bottom.

Downside scenario: stay out of the market, prices are low.

Helium market recommendations:

Buy: possible. Those who are in position from 900, keep stop at 770. Target: 2000.

Sale: no.

Support — 813. Resistance — 950.

Wheat No. 2 Soft Red. CME Group

Let’s look at the volumes of open interest in Wheat. You should take into account that this is three days old data (for Tuesday of last week), but it is also the most recent data published by CME Group.

At the moment there are more open short positions of asset managers than long ones. During the past week the difference between long and short positions of asset managers decreased by 4.4 th. contracts. Buyers and sellers were leaving the market. Sellers did it more actively. Bears are keeping control.

Growth scenario: we consider the March contract, expiration date March 14. Technically, we should buy here. But since we are already in a position, we recommend those who want to join the longs.

Downside scenario: let’s pause for a week.

Recommendations for the wheat market:

Buy: no. Who is in position from 533.0, keep stop at 527.0. Target: 635.0 (revised).

Sale: no.

Support — 533.2. Resistance — 551.6.

Corn No. 2 Yellow. CME Group

Let’s look at the volumes of open interest in Corn. You should take into account that this data is three days old (for Tuesday of last week), it is also the most recent of those published by the CME Group exchange.

At the moment there are more open long positions of asset managers than short ones. Over the past week the difference between long and short positions of asset managers increased by 29.5 thousand contracts. There are a lot of buyers. Sellers appeared, but they are few. Bulls have strengthened their control.

Growth scenario: we consider the March contract, expiration date March 14. We approach the resistance level at 488.0. Then 510.0. There’s nowhere to buy. Out of the market.

Downside scenario: the current area is interesting for selling. Selling from 510.0 is also possible.

Recommendations for the corn market:

Buy: no.

Sell: Now (486.4). Stop: 497.0. Target: 440.0. On approach to 509.0. Stop: 511.0. Target: 440.0.

Support — 474.0. Resistance — 495.0.

Soybeans No. 1. CME Group

Growth scenario: we consider March futures, expiration date March 14. We can keep longing for now. We are not expecting high levels, but we may reach 1100.

Downside scenario: refuse to sell for now.

Recommendations for the soybean market:

Buy: no. Who is in position from 1025.0, move the stop to 1030.0. Target: 1100.0.

Sale: not yet.

Support — 1016.2. Resistance — 1080.2.

Growth scenario: we consider the February futures, expiration date February 26. Once again, we have no guarantees of continued growth. Out of the market.

Downside scenario: approaching 2800. You should have already entered the short on Friday. If not, you can sell from current levels.

Gold Market Recommendations:

Buy: no.

Sell: no. Who is in position from 2790, keep stop at 2820. Target: 2000????!!!!

Support — 2734. Resistance — 2800.

EUR/USD

Growth scenario: the falling channel has been broken upwards. According to the classics, if we return to 1.0350, we will buy. Fed meeting on January 29th.

Downside scenario: we will refrain from selling for now.

Recommendations on euro/dollar pair:

Buy: when approaching 1.0350. Stop: 1.0290. Target: 1.1000 (1.2000?!).

Sale: no.

Support — 1.0349. Resistance — 1.0756.

USD/RUB

Growth scenario: we consider the March futures, expiration date March 20. Buying from the area of 95000 remains attractive. Long from current levels is possible.

Downside scenario: if we go below 101000, we can probably go to 95000. This scenario is better to work on hourly intervals.

Recommendations on dollar/ruble pair:

Buy: now (102242). Stop: 101400. Target: 114500. Think when approaching 95000.

Sale: no.

Support — 101534. Resistance — 103554.

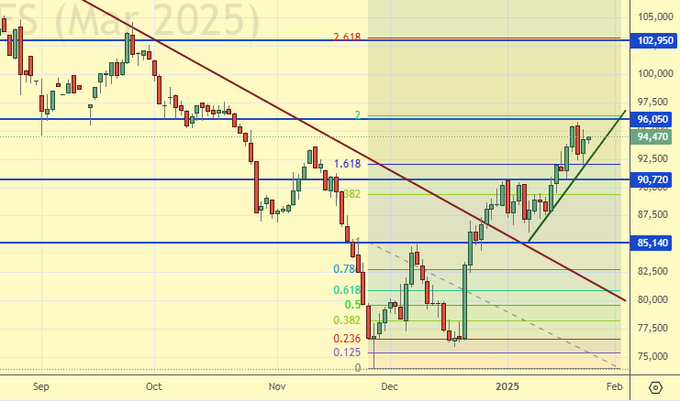

RTSI. MOEX

Growth scenario: we consider March futures, expiration date March 20. We’ve gone above 92000. It will be ugly if we go straight to 103000. But if we correct to 80000, we can consider buying from this level.

Downside scenario: the market maintains its tone. Selling from 103000 will look appropriate. Shorts from current levels are better to work out on hourly intervals.

Recommendations on the RTS index:

Buy: on a pullback to 80000. Stop: 78800. Target: 103000.

Sell: on approach to 103000. Stop: 104000. Target: 80000.

Support — 90720. Resistance — 96050.

The recommendations in this article are NOT a direct guide for speculators and investors. All ideas and options for working on the markets presented in this material do NOT have 100% probability of execution in the future. The site does not take any responsibility for the results of deals.